Invoicing EU companies as a UK business underwent changes post-Brexit, altering the VAT (Value Added Tax) rules and procedures. If you’re a UK business providing goods or services to EU companies, it’s crucial to understand the invoicing rules to ensure compliance with tax regulations in both the UK and the EU. Here’s a general guide:

1. VAT Registration:

- UK VAT: UK businesses should be registered for VAT in the UK if their taxable turnover exceeds the VAT threshold.

- EU VAT: If you sell goods or provide certain services in an EU country, you might need to register for VAT in that country. This can vary based on the nature of the goods or services provided.

2. Zero-Rated VAT on Services:

- As of post-Brexit rules, most services provided by UK businesses to EU businesses are zero-rated for VAT. This means you won’t charge UK VAT. However, the recipient may need to account for VAT in their country using the reverse charge mechanism.

3. Goods to EU:

- Zero-Rated VAT: Exports of goods from the UK to the EU can be zero-rated for VAT purposes.

- Custom Declarations: You’ll need to complete custom declarations for goods leaving the UK and entering the EU.

- Ensure your EU customer knows their obligations: They might have to pay import VAT and duties in their country.

4. Invoicing:

- Invoice in the currency of the customer: Though not a strict requirement, it can make the payment process smoother.

- Clearly state your VAT number and any EU VAT number you might have been assigned.

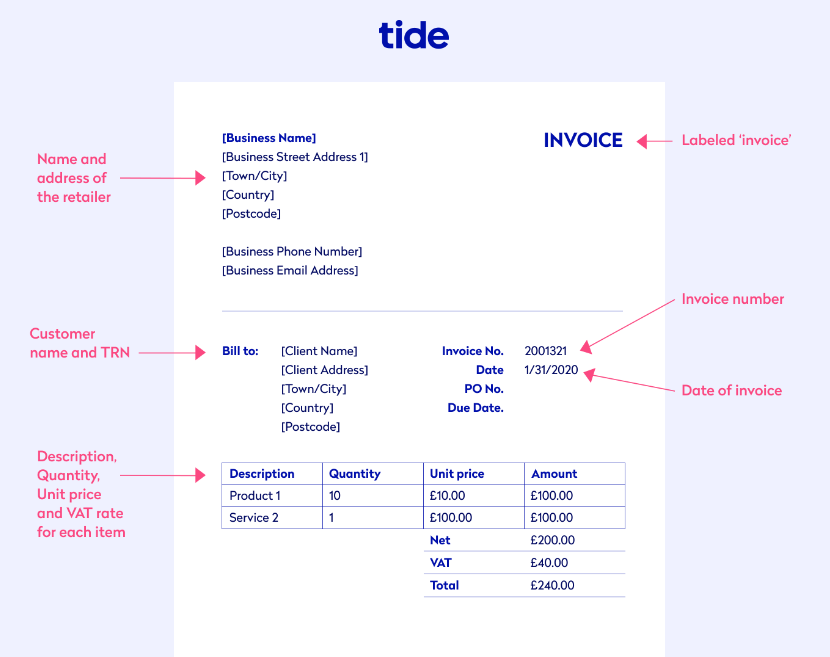

- Include all necessary details: Description of goods/services, date, invoice number, your business address, the customer’s address, and total amount.

- If you’re not charging VAT because the service is zero-rated, state the reason why, for example, “Reverse charge: Customer to account for VAT to the appropriate tax authority.”

5. Digital Services:

- For digital services provided to consumers (not businesses) in the EU, you might need to register for the VAT Mini One Stop Shop (MOSS) in an EU country or register for VAT in each EU country where you have consumers.

6. Store records:

- For VAT purposes, you must keep records of sales and any other relevant documentation for at least six years.

7. EC Sales Lists:

- Pre-Brexit, UK businesses had to complete EC Sales Lists for goods and services sold to EU businesses. Post-Brexit, this is no longer a requirement.

8. Always Stay Updated:

- Regulations can change. Monitor updates from both the UK government and the EU to ensure you remain compliant.

Conclusion: Invoicing EU companies post-Brexit requires an understanding of both UK and EU VAT regulations. It’s essential to keep abreast of updates, as regulations can evolve. Consulting with an accountant or tax advisor who specializes in international trade can provide clarity tailored to your business’s unique circumstances.